2026 Tax Changes in The Netherlands

The start of a new year often brings tax changes that can affect your income, savings, property, or business in ways that are easy to overlook. For 2026, the Dutch tax system will see several adjustments, ranging from small shifts in tax brackets and credits to more impactful changes for investors, property owners, and entrepreneurs. While many of these updates are technical in nature, together they can influence how much tax you pay and which financial planning opportunities may still be available for you. Below, we highlight the most important tax changes for 2026 and explain what they could mean for your situation.

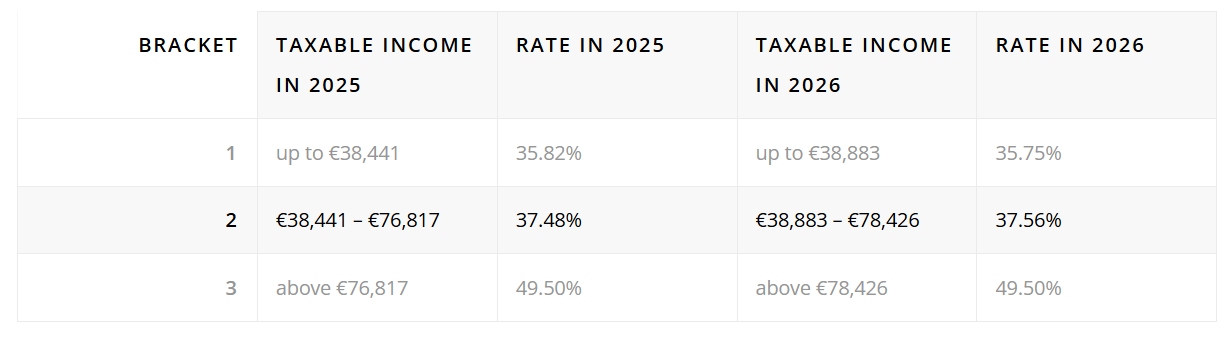

Changes in Box 1

The table below provides an overview of the income tax brackets (Box 1) for 2026, compared with those for 2025. While the structure of the tax system remains unchanged, both the bracket thresholds and tax rates shift slightly due to annual indexation and policy adjustments. In 2026, the lower bracket increases modestly, and the rate in the first bracket decreases slightly, offering minimal relief for lower and middle incomes. The second bracket becomes slightly wider, with a small rate increase. The top rate of 49.50% remains unchanged, though the threshold at which it starts moves upward.

Overall, these changes are relatively limited but may still result in small differences in your net income, depending on your salary level and personal tax situation.

If you have reached the AOW age in 2025, the following tax brackets and rates will apply for 2026:

Please note: The table above applies to individuals who reach AOW age in 2026, born on or after 1 January 1946. For other ages, it is best to check with the Dutch Tax Authorities for the applicable rates.

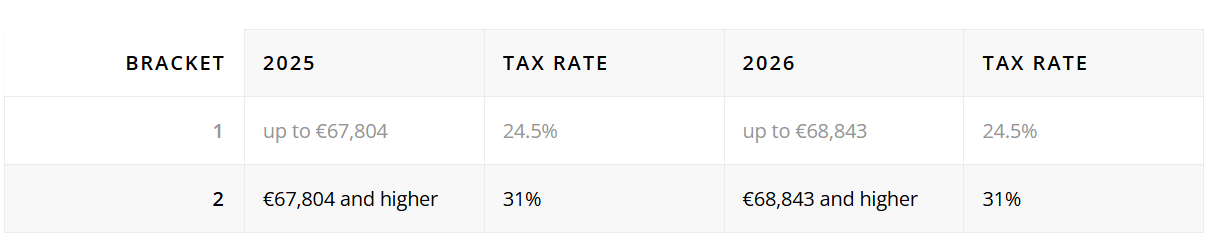

Changes in Box 2

The Box 2 tax rates remain unchanged in 2026, but the bracket thresholds are slightly increased due to indexation. This means that in 2026 you can receive a bit more income from substantial interest at the lower 24.5% rate before moving into the higher 31% bracket. The threshold for the first bracket increases by €1,039, from €67,804 in 2025 to €68,843 in 2026. Any income above this amount falls into the second bracket. For fiscal partners, an additional advantage applies: both partners may use the first bracket individually. As a result, a combined dividend distribution or capital gain in 2026 can be more tax-efficient, because a larger portion of the income can be taxed at the lower 24.5% rate.

Changes in Box 3

The tax-free allowance for Box 3 is increased from €57,684 in 2025 to €59,357 in 2026. The fictitious return on other assets in Box 3 grows from 5.88% in 2025 to 6% in 2026. This concerns assets that are not held in a bank account. In addition, the deemed returns for bank accounts (1.28% in 2026) and debts (2.70% in 2026) also change.

If the deemed return in Box 3 is higher than the actual return you earned, you can use the OWR form (Opgaaf Werkelijk Rendement) to challenge it. This form allows you to demonstrate that your real return was lower than the notional return calculated by the tax authorities. If accepted, you will not be taxed based on the (often higher) fictitious return but on your actual income instead. This can lead to significant tax savings, especially for savings, investments, or real estate in Box 3.

Changes for entrepreneurs and companies

Businesses and entrepreneurs will also see several notable changes in 2026. One key adjustment is the tightening of the lucrative interest regime, specifically aimed at private equity managers. Until now, they paid less tax on the wealth they accumulate through their remuneration structures than individuals who are taxed in Box 3. The government considers this difference undesirable. Therefore, the rules are being amended so that the tax burden in Box 2 for this group will align with the Box 3 rate of 36%. As a result, private equity managers will face a higher tax burden on their lucrative interests in 2026.

The self-employed tax deduction will be reduced from €2,470 in 2025 to €1,200 in 2026. In addition, the Dutch Supreme Court ruled in March 2025 that companies may deduct more losses when liquidating subsidiaries. This ruling creates a financial setback for the government. To compensate for this, the Aof premium, the employer contribution used to fund disability schemes such as WIA and WAO, will be increased by 0.08% in 2026. Employers will therefore face higher labour costs.

Finally, it has been announced that the rules regarding currency gains on participations will be updated, but this adjustment will not take effect until 1 January 2027. Nothing changes in this regard for 2026, but businesses may want to prepare in advance for this future policy shift.

Gift tax changes

The gift tax exemptions increase slightly in 2026 due to annual indexation, giving you a bit more room to make tax-free gifts, unlike in 2025. The standard annual exemption for gifts from parents to children rises from €6,713 to €6,908, while the exemption for gifts to others increases from €2,690 to €2,769. The one-time higher exemptions for children aged 18 to 40 also go up: €33,129 for general purposes and €69,009 for education in 2026.

Inheritance tax changes

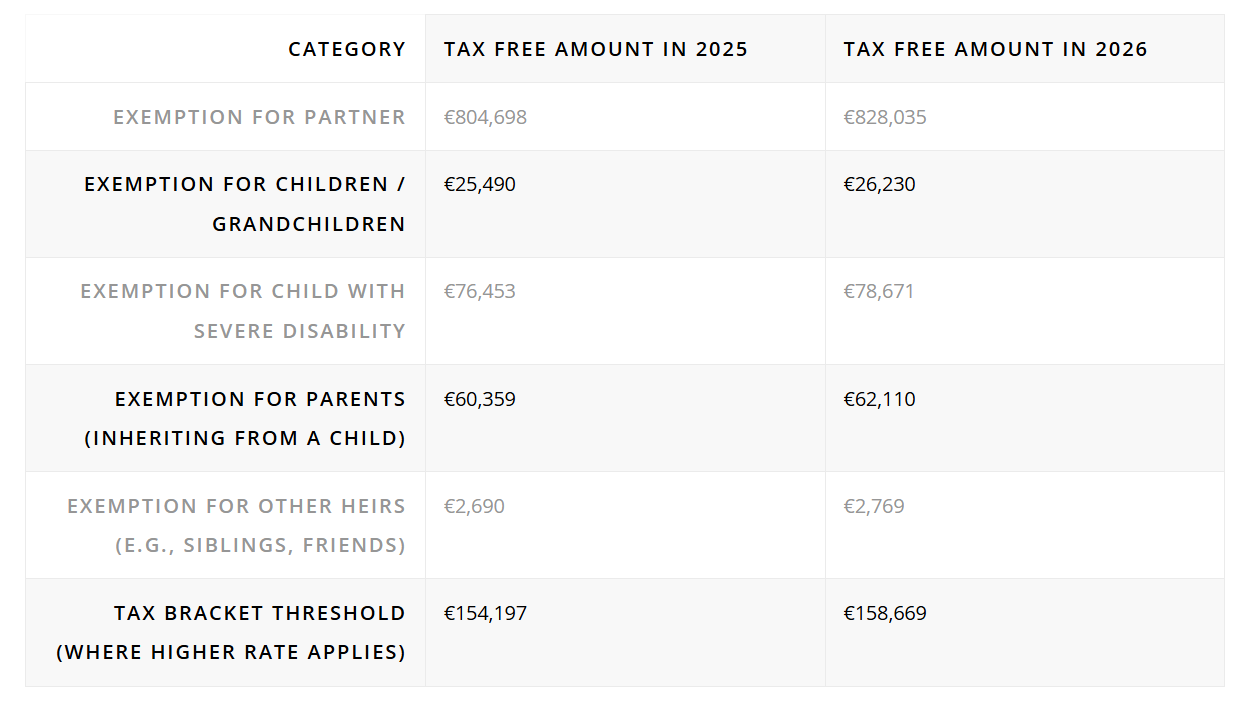

The inheritance tax thresholds grow in 2026 due to indexation, giving heirs a bit more tax-free room. The exemption for partners rises significantly, from €804,698 to €828,035, while the exemptions for children, grandchildren, parents, and other heirs also increase but modestly. In addition, the threshold at which the higher inheritance tax rate applies is raised from €154,197 to €158,669. Although the tax rates themselves remain unchanged across all categories, these higher exemptions and bracket thresholds mean that in 2026, a larger portion of an inheritance can be received tax-free or taxed at a lower rate.

Changes in tax credits and deductions

The general tax credit icnreases slightly, from €3,068 in 2025 to €3,115 in 2026. The employed person’s tax credit also changes: the maximum amount rising from €5,599 to €5,712. The income-related combination tax credit (IACK) grows to €3,032, a modest adjustment compared to €2,986 in 2025. The tax credit for young disabled persons will also be increased slightly, from €909 to €923.

However, the biggest change will affect entrepreneurs. The self-employed tax deduction will be further reduced and will fall sharply: from €2,470 in 2025 to €1,200 in 2026.

Tax changes on Box 3 properties and owner-occupied homes

In 2026, the owner-occupied home rate (eigenwoningforfait) remains unchanged at 0.35% of the WOZ value, just as in 2023, 2024, and 2025. What does change is the threshold at which the higher rate applies: this shifts from €1,330,000 in 2025 to €1,350,000 in 2026. Above this threshold, the higher rate of 2.35% continues to apply.

For properties classified in Box 3, two important changes take effect in 2026:

- First, the transfer tax for properties not used as a main residence is reduced from 10.4% in 2025 to 8% in 2026.

- Second, the rules for applying the leegwaarderatio (the valuation discount for rented properties) are significantly tightened. Up to and including 2025, the leegwaarderatio could be applied to almost any rental situation, whether the rent is market-based or not, and even when renting to related parties such as family members or your own company. This can substantially reduce the taxable Box 3 value of a rented property. Moreover, under a Dutch Supreme Court ruling, you are still allowed to use an even lower value if you can prove that the real market value is at least 10% below the WOZ value after applying the leegwaarderatio, supported by objective evidence. From 2026 onwards, these rules got stricter. The Supreme Court ruling will be codified in law, meaning the option to use a lower actual value remains available but is formally embedded. The most significant change is that the leegwaarderatio may no longer be applied if the rent is not at arm’s length. In addition, when a property is rented to a related party, the leegwaarderatio will be disallowed if the rent deviates from what independent parties would reasonably agree. Only when related parties rent at a market-conforming price can the discount still be applied.

This means that if you rent a property to family members or to your own company at a below-market rent, you will no longer be allowed to use the leegwaarderatio from 2026 onwards. The property will then have to be valued at the full WOZ value in Box 3, which can significantly increase the tax burden. For that reason, it is advisable to check whether the rent you charge in such situations is truly market-based.

Conclusion and advice from TaxSavers

The tax changes for 2026 consist mostly of small adjustments, but together they can still affect your financial situation. The tax bands and rates in Box 1 and Box 2 shift slightly, which means your income may be taxed differently than before. In Box 3, the tax-free allowance will be increased, and the deemed return on investments and other assets will increase, particularly for investors.

There are also several relevant changes related to housing. The imputed home value (eigenwoningforfait) remains the same, although the threshold for the higher rate shifts slightly. For property investors, the impact is greater: the transfer tax for Box 3 properties will be reduced, while the rules for applying the valuation discount (leegwaarderatio) become stricter, especially when renting to family members or other related parties. Entrepreneurs will also notice changes, including the continued reduction of the self-employed deduction.

While none of these adjustments are dramatic on their own, their combined effect may influence your overall tax burden. It’s therefore worthwhile to review how the new rules apply to your situation and to consider whether any steps are needed to make the most of the tax opportunities available in 2026.

Would you like help saving as much tax as possible? TaxSavers team is here to assist you. We can help reduce your Box 3 tax burden and provide personalised advice on your financial situation, for example, if you have recently purchased a home or received a gift. Visit our website to explore the services we offer. You can send an email to us at info@taxsavers.nl, give us a call, or WhatsApp us at +31 020 217 0120 to discuss your situation with one of our specialists!