Saving or Investing: What Really Happens to Your Purchasing Power?

For many people living in the Netherlands, saving money feels natural. That is not a coincidence. After the Second World War, Dutch households were strongly encouraged to save. Government initiatives and youth savings schemes helped rebuild financial stability and laid the foundation for a culture of disciplined saving. This mindset later contributed to one of the strongest pension systems in the world: regular contributions, long time horizons, and patience.

Saving still has an important role today. Money held in a savings account offers security, flexibility and certainty. Funds remain accessible and the value does not fluctuate. For short-term goals or emergency reserves, this stability is essential.

However, when we look at purchasing power over longer periods, the picture changes.

Let us compare two simple scenarios. In both cases, the same fixed amount is deposited every month over many years. One scenario uses a traditional savings account; the other uses an investment account diversified across financial markets.

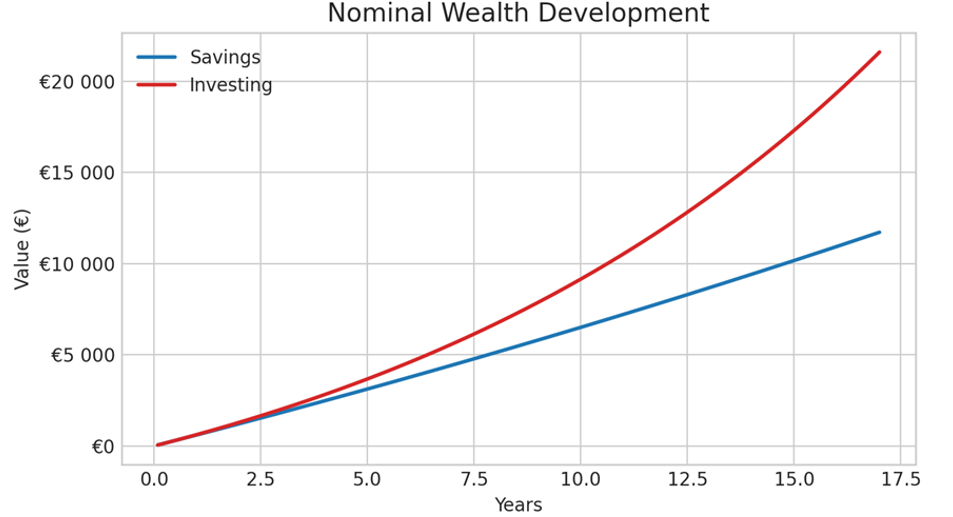

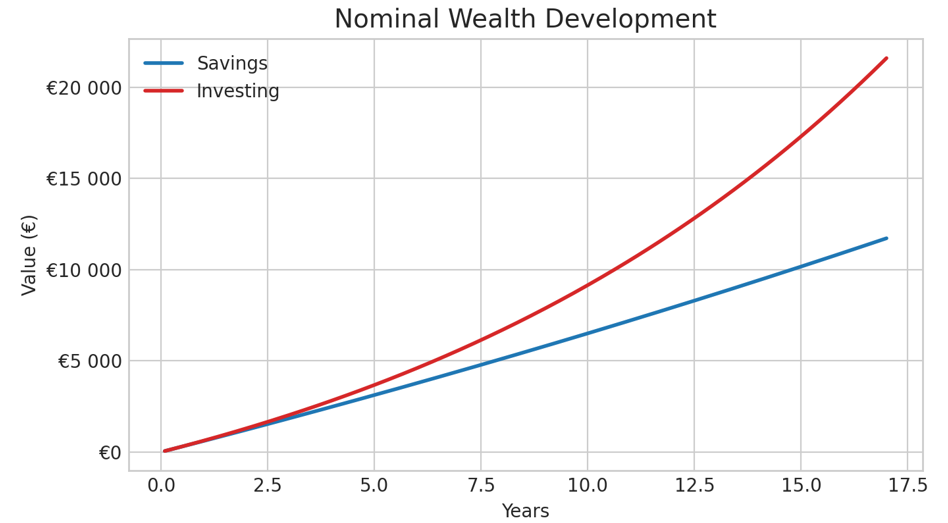

A first graph shows the development of nominal wealth. The savings line rises steadily and predictably. The investment line moves up and down — sometimes sharply — reflecting market fluctuations. This volatility often explains why people feel more comfortable saving.

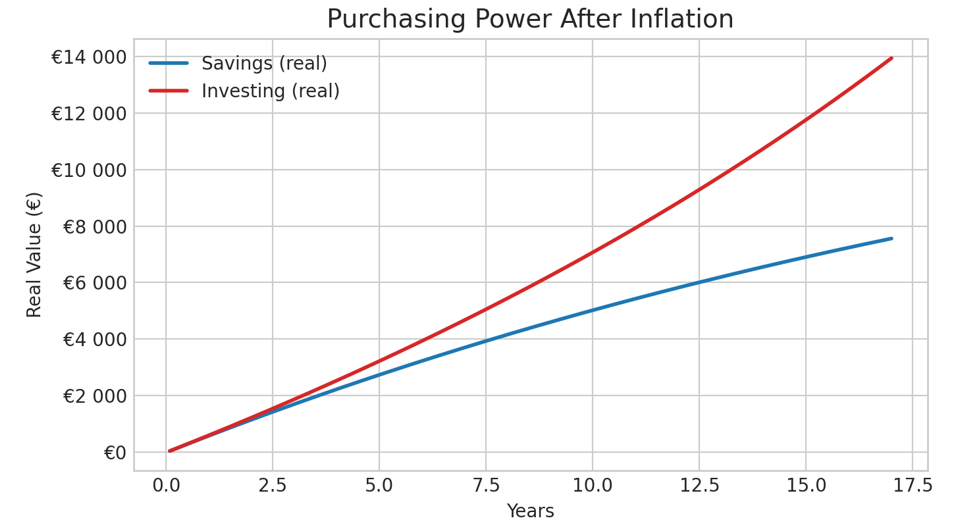

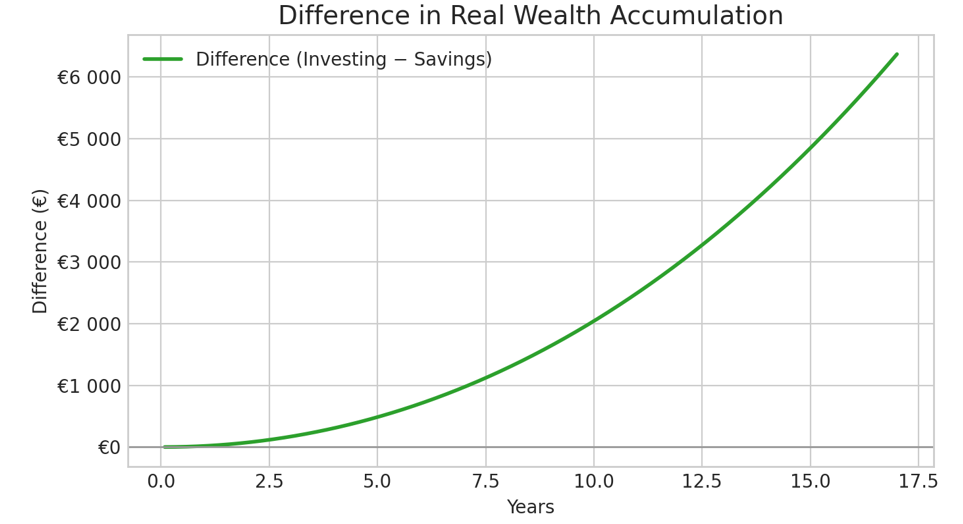

A second graph tells the more important story: purchasing power after inflation. Here, the savings line gradually flattens. Even though the balance grows, rising prices reduce what that money can actually buy. The investment line, despite temporary declines, shows stronger long-term growth because returns historically outpace inflation over extended periods.

The key difference lies in risk and time. Investment returns exist because investors accept uncertainty. When money is needed soon, taking significant risk is usually inappropriate. But when the horizon is long, for example retirement planning or building wealth for children, time helps smooth market fluctuations and increases the likelihood of higher real returns.

This does not mean saving is outdated. On the contrary, savings and investments serve different purposes. A healthy financial plan typically combines both: savings for stability and accessibility, investments for long-term growth.

For internationals living and working in Leiden, this distinction is especially relevant. Financial systems, habits and pension arrangements differ widely between countries. Understanding how regular monthly contributions affect future purchasing power can make a significant difference to long-term financial security.

In short: saving protects today’s certainty, while investing helps protect tomorrow’s lifestyle. The right balance depends on your goals, your time horizon and your comfort with risk.

Assumptions used in the graphs: €50 deposited monthly for 17 years; historical average savings rate 1.6% p.a.; investment return 8% p.a.; inflation 2.58% p.a. Values compounded monthly and real values adjusted using the same inflation.